.png)

Yield and DeFi are two of the most prominent words in the era of crypto renaissance. Renaissance as a period in history is described as the time of innovation, growth and prosperity, built on the renewed interest in classical advancements. In this article, we look back at the brief but turbulent history of DeFi and on-chain yield. We explore the classical models that current DeFi builds upon, and highlight both the innovations and drawbacks as they happened.

The acronym DeFi stands for Decentralized Finance. Decentralized means that it happens purely on-chain, backed by blockchains as decentralized ledgers. DeFi builds on and ideally retains the properties that we typically quote along with decentralized systems: self-custody, trustlessness, and censorship-resistance. Self-custody means that individuals have the ability to hold and store value and its representation. Trustlessness means that they can interact with each other and other systems in DeFi without the need for a trusted intermediary, and censorship resistance means that they cannot be prevented from doing so.

Blockchains allow us to implement systems that achieve all of the above. They form the backbone of the financial peer-to-peer economy that DeFi creates. From a software architecture point of view, DeFi is part of the application layer built on top of blockchains.

We consider MakerDAO to be the first DeFi protocol due to its origins going as far back as 2015, despite the whitepaper titled The Dai Stablecoin System not being published until December 2017. It introduced Single Collateral Dai as the first stable coin that everyone was able to mint. In simplicity, anyone could interact with a smart contract in the MakerDAO system, deposit Ether as collateral, and receive stable coin DAI pegged to the US dollar. This makes MakerDAO the first widely adopted collateralized debt position (CDP). In exchange for providing Dai, MakerDAO charged users a stability fee, taken at time of repayment. This stability fee accrued to the protocol, which as its name implies, was used for maintaining the peg of DAI.

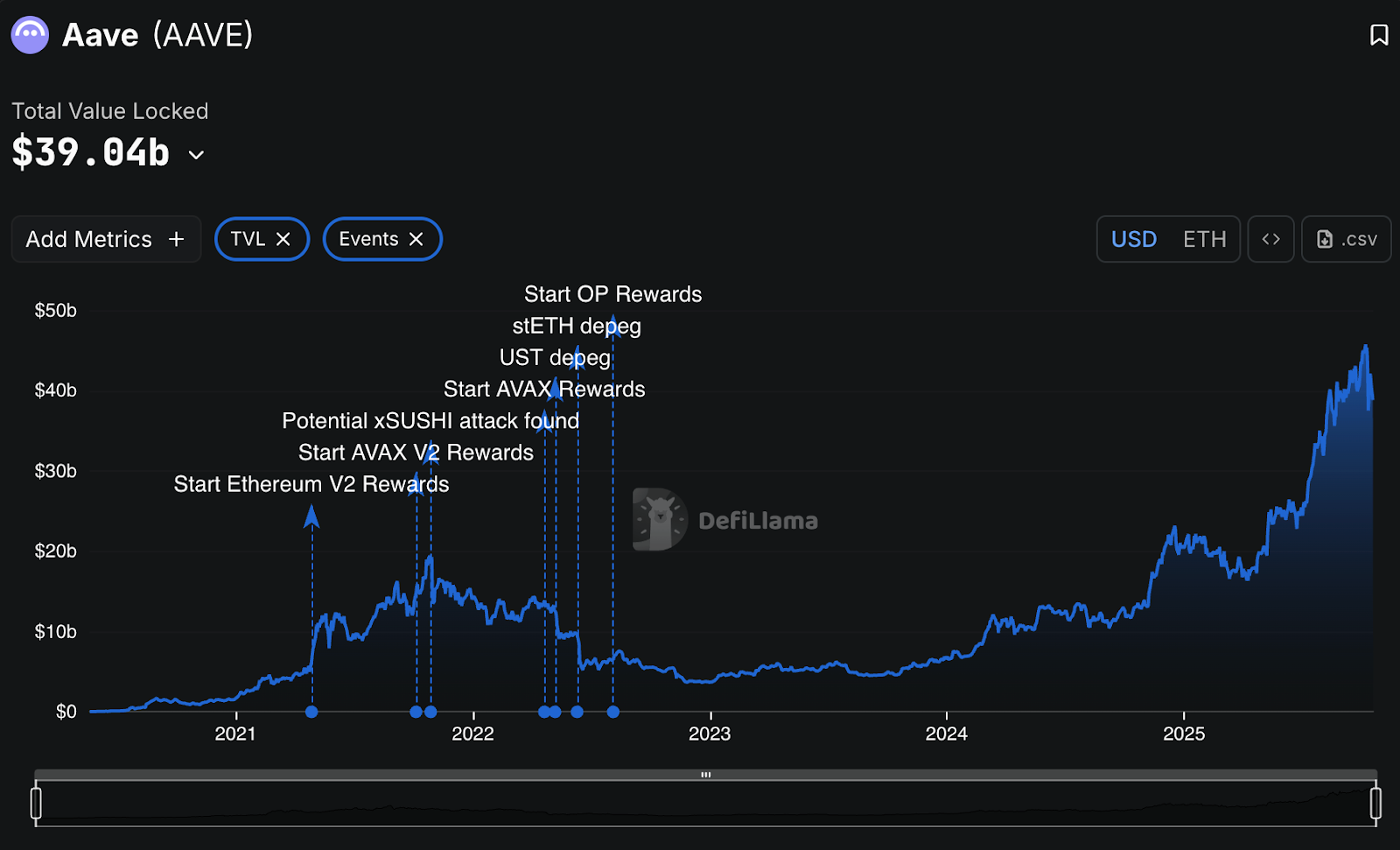

The early MakerDAO protocol was primarily a leverage engine rather than a yield engine. The primary motivation to mint DAI was to access liquidity without selling exposure to the underlying ETH. The traditional lending products that generate yield for the lenders originate elsewhere. ETHLend (now well-known as Aave after it changed its mechanics and rebranded in 2020) was deployed in November 2017. ETHLend was a peer-to-peer (P2P) lending marketplace. Instead of using liquidity pools (like Aave or Compound later did), it directly matched individual borrowers and lenders through smart contracts. Borrowers created loan requests specifying the amount of ETH they wanted to borrow, the collateral token they would lock up, the loan duration and interest rate. Lenders could browse open loan requests and choose which ones to fund. Loans were over-collateralized, usually at 150% or more, to protect lenders from borrower default. If the borrower failed to repay within the agreed period, the smart contract automatically transferred the collateral to the lender; no intermediaries needed.

There were no credit scores, only on-chain collateral as security, similar to MakerDAO.

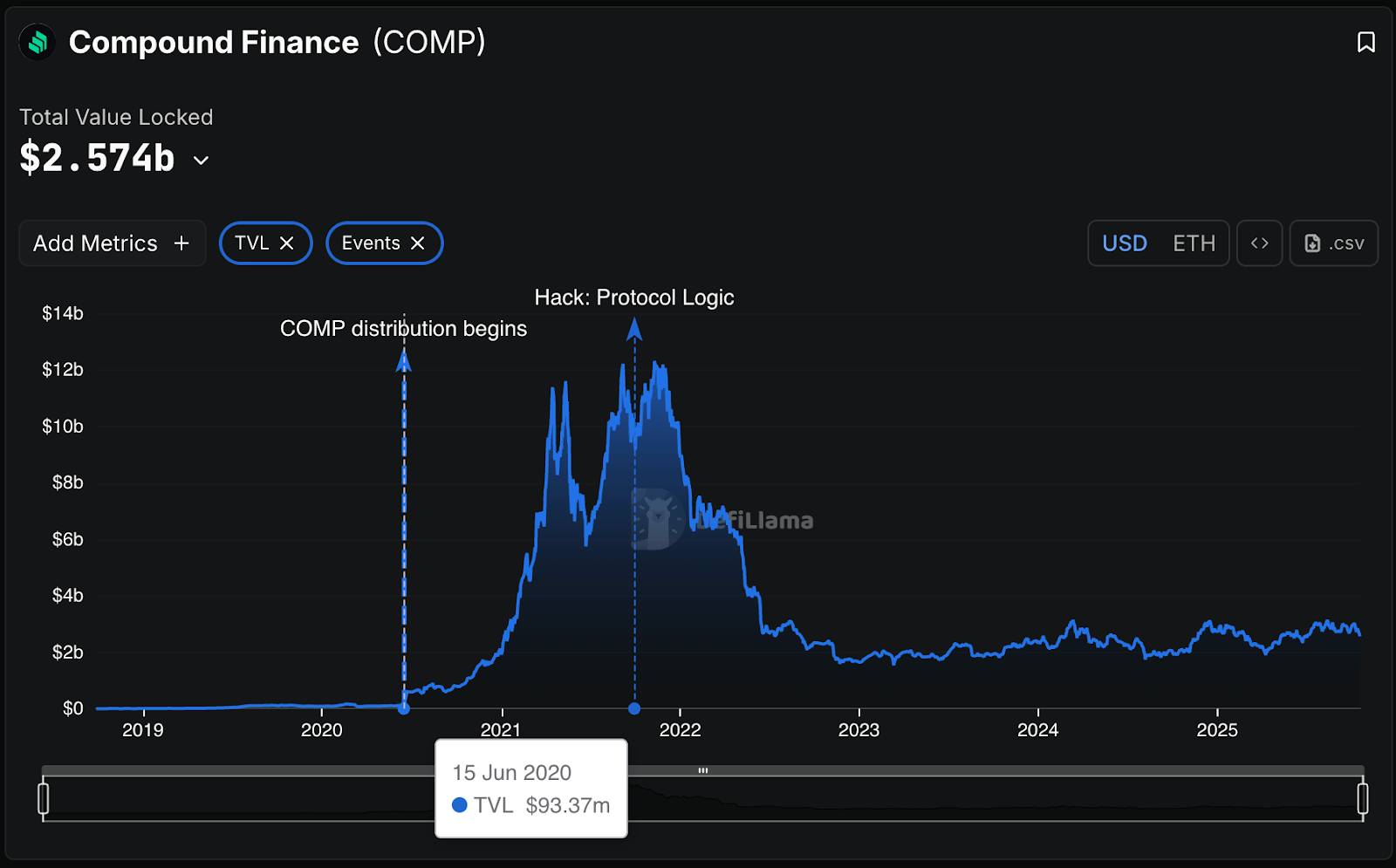

An early competitor to ETHLend emerged in the form of Compound. The innovation of Compound over ETHLend was the model based on liquidity pools, rather than peer-to-peer request matching. Individuals were able to contribute a variety of major assets to the liquidity pools, and borrow other assets against their collateral. The interest was driven by a curve rising with the increasing utilization of the pool. Compound continued to innovate in the DeFi space: in 2019, it was the first to introduce yield bearing receipt tokens (cTokens) for deposited liquidity. cTokens became the first widely adopted implementation of on-chain freely transferable yield-bearing tokens, which is the concept that enables composability of DeFi, giving rise to the notion of “money legos.” In 2020, it introduced the concept of liquidity mining by distributing its own governance token COMP.

The adoption of lending in the early days of DeFi remained low compared to the current standards. Compound’s TVL barely surpassed $100m prior to June 2020, and it is only about 0.25% of the current TVL of Aave which, at the time of writing, exceeds $39B.

On the other hand, Ethereum has always seen strong demand for trading products. The network introduced the ERC20 standard for creating new digital tokens, which was heavily used in the ICO era peaking in 2017. Ethereum also always had its own native asset Ether (ETH) used to cover transaction fees, there was an abundance of ICO tokens, and with MakerDAO, it also had a decentralized stable coin, all of this waiting to exchange hands.

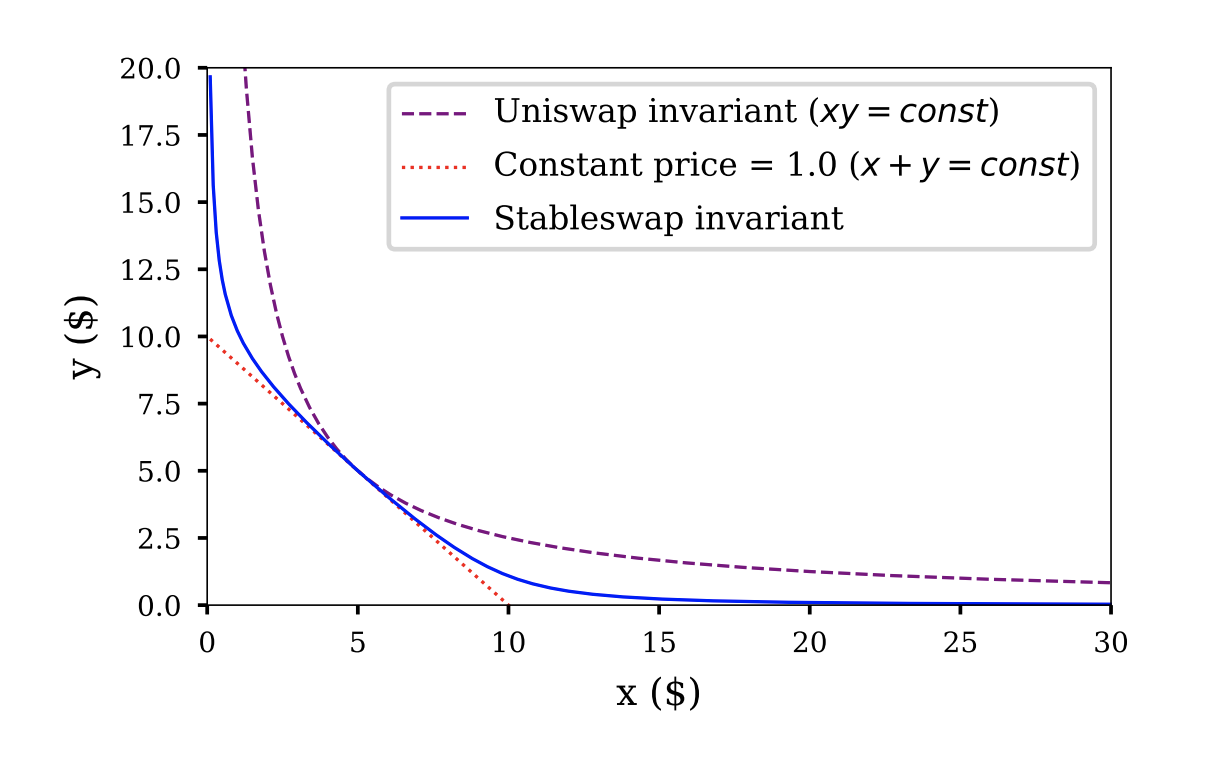

In 2017, Bancor introduced the concept of an on-chain liquidity pool that automatically prices tokens using a formula. It allowed users to swap tokens directly against a smart contract instead of relying on order matching with a counterparty. This was the first implementation of an automated market maker (AMM) model on Ethereum. Bancor used the so-called Constant Reserve Ratio (CRR) pricing formula. Uniswap, deployed in November 2018, built on and simplified Bancor’s ideas, using the constant product formula (x * y = k) introduced in 2017 by Vitalik Buterin’s blog post.

Uniswap’s gas-efficient implementation led to an explosive adoption and became the dominant AMM design. Instead of order book matching, the AMMs work with liquidity pools. In simplicity, individuals, so-called liquidity providers (LPs), deposit assets into liquidity pools, and are willing to fulfill trades between those assets at a price that is fair to the market. The fair price is determined by a mathematical formula (often visualized as a curve) based on the ratio of assets in the pool. As an asset becomes scarce, it appreciates in value compared to the other asset. Anyone can then come to the pool, initiate a trade, and get payout based on the formula. The liquidity providers get a fee charged on the trade volume.

Curve Finance launched in early 2020, and was a modification of the classic AMM model. Rather than using x * y = k constant product curve, it utilized a specialized curve called the stableswap invariant. This curve utilizes a constant sum invariant x + y = k at a widened middle range, ensuring lower slippages and better execution for “stable,” pegged assets, while significant imbalances caused by large swaps push the curve towards the constant product model. This innovation made Curve the go-to liquidity hub for stablecoins, which set the stage for later developments like the Curve Wars.

Later versions of Uniswap introduced concentrated liquidity, which allowed LPs to deploy capital within specific price ranges (denoted by a range of ticks) for better efficiency, potential profitability, and reduced impermanent loss.

The drawbacks of DeFi and decentralized systems exhibited themselves on March 12, 2020, which is the date known to the DeFi community as Black Thursday. As the markets reflected the fears of the impending global pandemic, the price of both BTC and ETH crashed nearly 40% in a single day. The sudden selloff led to Ethereum network congestion and skyrocketing gas fees.

MakerDAO’s Single-Collateral DAI (Sai) and newly launched Multi-Collateral DAI (MCD) were heavily impacted. ETH dropped from roughly $190 down to $90 within hours, and MakerDAO’s collateralized debt positions, now called Vaults, suddenly became undercollateralized.

Maker’s liquidation system triggered mass liquidations to restore solvency. However, most liquidation bots failed to participate. Some attribute it to the network congestion, but the reality is that there were not so many bots running to participate in the auctions in the first place.

Some liquidators exploited the situation and won auctions with bids of 0 DAI for a vault of collateral, because there were no appropriately priced competing bids.

As a result, collateral was seized for free, and MakerDAO was left with around $4.5 million USD in bad debt. In order to rectify the situation, MakerDAO governance voted to mint and auction new governance tokens (MKR) to recapitalize the system. Additionally, new collateral types such as USDC to stabilize DAI’s peg, and MakerDAO also improved the liquidation mechanisms.

The events of Black Thursday highlighted the drawbacks of DeFi. Sudden market movements have secondary effects in the DeFi ecosystem, which can amplify as the funds loop through protocols. Secondarily, the decentralization in DeFi does not guarantee liveness and participation. The lack of participation in the auction showed the need and resulted in creating protocols such as KeeperDAO, a cooperative liquidity layer coordinating on-chain so-called “keepers”, the bots that execute profitable opportunities like liquidations, arbitrage, and rebalances.

Big things started brewing for DeFi in June 2020, when Compound realized that the economic incentives for lending did not have to come solely from the borrowing fee. It could be subsidized with token incentives, where protocol tokens could be distributed as a reward for supplying liquidity. This clever bootstrapping solution became known as “liquidity mining”.

LPs soon realized that they could achieve APYs on the order of 10x by recursively borrowing and redepositing to farm liquidity mining token incentives. This is one of the earliest cases of what we know today as a classic example of “yield looping.” This era soon became what we now know as the “DeFi summer.”

The success of Compound’s liquidity mining program spurred many similar liquidity mining programs across the DeFi landscape. Soon, yield farmers were constantly rotating their capital between various protocols, recursively farming yields, leading to mass token inflation and impermanent loss in volatile pools on AMM DEXs like Uniswap. By late 2021, most protocols had followed suit and adopted liquidity mining programs.

Yield farming had become a crypto primitive that the people demanded, and it was here to stay. However, navigating the landscape of incoming protocols, understanding their liquidity mining program, and evaluating risks remained a task equivalent to a full-time employment. Furthermore, most of the protocols with liquidity mining incentives were present on Ethereum’s mainnet, which meant that the yield farmers often needed to weigh whether the gas fees, primarily those for collecting and liquidating profits, are worth realizing the gain.

Therefore, yield farming vaults emerged in 2020 to automate this chaos, and pool assets to increase the efficiency of the principal when realizing gains. Protocols like Yearn Finance and soon after, an early competitor Harvest Finance, algorithmically shifted funds across money markets such as Aave and Compound, autocompounding at periodic intervals to capture compounded returns. They became an automation tool, as well the first yield abstraction layer that socialized the costs of harvesting and compounding. As a result, APYs on stables surged, reaching upwards of 30%.

The yield farming protocols were so remarkably utilized that they managed to develop their own ecosystems. Yearn Finance was particularly active in this domain, and through a series of mergers and acquisitions, adopted protocols such Cream Finance for lending of assets that were not supported on major lending markets on Compound and Aave, Sushi Swap fulfilling the role of an AMM DEX, and even Iron Bank for protocol-to-protocol lending.

As the vault model matured, so did the strategies that these vaults were built on. In 2021, Yearn V2 introduced multi-strategy vaults. Strategies were no longer contained to simple reallocation of LP capital to different money markets. Instead, they began to be used for complex strategies, such as flash loan-facilitated arbitrage.

In 2020, ETHLend rebranded to Aave and launched a new protocol based on the liquidity pools. The protocol contained many upgrades, including so-called flash loans. In simple terms, a flash loan is an uncollateralized loan that one can take from a smart contract for the duration of a single transaction. If the loan does not get repaid at the end of the transaction including the appropriate fees, the smart contract will revert the entire transaction. Therefore, one can possibly borrow all the capital available in the pool. Flash loan functionality is nowadays a part of many popular DeFi protocols, including Uniswap.

The primary intention of flash loan support was to provide arbitrage searchers with enough funds to realize any kind of arbitrage opportunity. However, the amounts available as loans were largely sufficient to manipulate the liquidity pools of DEXes and other protocols. The increased complexity of strategies in yield aggregators’ funds looping through money legos had increased the attack surface. Therefore, this era is also marked by a large number of hacks and losses in DeFi protocols. The Harvest Finance exploit in late 2020 utilized flash loans to manipulate the prices of the underlying assets in a vault, and consequently the withdrawal ratios of these assets. It halted the rapid expansion of the protocol, and clearly demonstrated that the vault security was not contained to the vault contract code itself, but expanded far beyond to the interaction with the entire DeFi ecosystem. Yearn Finance also sustained multiple exploits and lost millions. During this time of rapid innovation, these types of exploits were typical and not uncommon, nor contained to the protocols listed thus far.

The liquidity mining mechanic was used in late August 2020 and early September 2020 in a rather literal sense by an incoming protocol called SushiSwap. At the time Uniswap was dominating the DEX market. However, Uniswap had no governance token yet, as its UNI token didn’t exist until late September 2020. An anonymous developer called Chef Nomi forked Uniswap’s open-source codebase and created SushiSwap by offering a liquidity mining program that Uniswap was missing. For about 10 days, the LPs could deposit Uniswap’s LP token into SushiSwap, and receive the governance token SUSHI as an incentive. The promise was simple: once SushiSwap launched its own exchange, all the Uniswap liquidity tokens staked in the contract would be migrated to SushiSwap’s own pools, along with their liquidity. Therefore, the event now known as the SushiSwap “vampire attack” on Uniswap is one of the most famous and controversial events in DeFi history. In response, Uniswap airdropped its UNI token retroactively in September to past users to attempt to regain market share lost to SushiSwap. This sparked the trend of airdrop farming, where users interacted with protocols in hopes of future token rewards.

While SushiSwap’s origin story was the vampire attack on Uniswap, it was not just a Uniswap fork. It was a new AMM architecture that was forked many times over. PancakeSwap on BSC forked SushiSwap’s MasterChef staking contract for liquidity mining – the same liquidity mining contract that was used in the vampire attack on Uniswap. Eventually, SushiSwap was integrated into the Yearn ecosystem and expanded to include products such as BentoBox for lending and Kashi, built on top of BentoBox, for isolated lending.

The creation of yield-bearing tokens by protocols like Yearn and Curve created a new primitive: interest-bearing collateral. This new primitive resulted in the next-generation vault model, which capitalized on the recognition that yield-bearing tokens were productive assets that were sitting idly. The Abracadabra protocol launched in June 2021 functioned similarly to the MakerDAO CDP model, but allowed yield-bearing vault tokens as collateral. Users were able to deposit assets like Yearn USDC (yvUSDC), which was already earning upwards of 15% APY, into Abracadabra “Cauldrons” to mint Magic Internet Money (MIM), a stablecoin. Other yield-bearing forms of collateral, such as SushiSwap’s yield-bearing governance token xSUSHI, were supported too.

Abracadabra’s interface allowed users to achieve significant leverage on already high-yielding stablecoin positions with a single click. Users would deposit a yield-bearing stablecoin like yvUSDC into a cauldron to mint MIM, which was then swapped into USDC and redeployed into Yearn for yvUSDC, which was then redeployed into the yvUSDC Cauldron and repeated.

This strategy became immensely popular and drove massive TVL inflows into both Yearn and Abracadabra (peaking at >US$6B TVL each) and represented a local peak in capital efficiency using existing vault primitives. This strategy introduced significant systemic risk, however. It relied heavily on MIM peg stability and liquidity. If MIM depegged, the looping strategy would rapidly unwind and lead to heavy liquidation cascades.

These systemic risks remained in the shadows, however, until the notorious LUNA/TERRA crash of May 2022. An L1 that was little known for a period of time, Terra surged in popularity with the introduction of their algorithmic stablecoin, UST, which was tied to its sister token LUNA to maintain its peg.

Before we mention the stablecoin atmosphere at the time, let’s define what an algorithmic stablecoin is. Up until the period of UST dominance, most stablecoins were full or overcollateralized stablecoins. By full collateralization we mean that to mint $1 of a stablecoin, an individual needs to deposit $1 of a collateral asset. Similarly, with overcollateralization, an individual needs to deposit >$1 of a collateral asset to mint $1 of a stablecoin, where the amount required depends on the collateralization ratio specified by the stablecoin.

In contrast, algorithmic stablecoins were stablecoins that relied on algorithms to maintain their peg, some using partial collateralization and others relying fully on algorithmic strategies with no collateral required. These algorithms were designed to incentivize users to arbitrage assets in the algostable machine to re-peg the stablecoin when its price deviated from the intended stable price.

Those active in the DeFi space at this time remember purely algorithmic stablecoin models such as Empty Set Dollar (ESD) and Basis Cash (BAC), both of which failed spectacularly. These systems relied on complex coupon/debt mechanics that users did not understand, and which had no incentive or poorly designed, weak incentives for users to support the peg when the peg broke.

Terra/Anchor surged in popularity because it provided a clear, simple use case, hiding its underlying algorithmic risks while also providing unmatched yields relative to other stablecoin yield machines. It was a dual-token model, where UST relied on mint and burns of its sister token, LUNA, to maintain its peg.

Anchor borrowers were subsidized in Anchor’s native token, ANC, encouraging heavy borrowing. At the same time, high APYs on UST deposits incentivized heavy lending, encouraging borrowing against bonded assets as collateral. This resulted in significant UST minting via burning LUNA, effectively reducing LUNA’s supply and sustaining the high yields on UST. It seemed like everyone won here; high yields drew UST deposits, increasing demand for borrowing and collateral staking, resulting in collateral appreciation and greater overall yield.

Depositors minted aTokens (such as aUST for UST deposits), which represented a user’s deposit. These aTokens were redeemable at any time, giving the illusion of low depositor risk. The Terra/Anchor flywheel was entirely dependent on constant inflows and token subsidies from the Terraform Labs yield reserve. When these halted, projected APYs tanked and mass instantaneous withdrawals resulted in the failure of UST, which relied on LUNA/UST arbitrage to maintain its peg. Simultaneously, LUNA failed, which relied on high APYs of UST to sustain its value.

The crash of TERRA/LUNA highlighted systemic overexposure and leverage, which turned out to be catastrophic. UST, with its high yields, was the de facto “risk free” rate provider and was used as collateral throughout the DeFi landscape. When UST failed to maintain its peg, liquidation cascades spread like wildfire, wiping out billions in value - this marked the beginning of what we now know as “DeFi Winter.”

As traders, investors, and institutions alike lost billions of dollars, the Web3 space displayed remarkably low levels of trust, leading to historical lows for token prices, ICO participation, and liquidity provision. Almost anything crypto saw a sharp decline - there was simply no more capital left to deploy, and any capital spared was promptly off-ramped.

At the end of March 2021, OlympusDAO popularized the concept of (3,3) to describe cooperative behavior between users and the protocol using a game-theoretic payoff matrix. OlympusDAO sought to solve what it saw as the core weakness of DeFi 1.0 liquidity mining models – the “mercenary capital” problem. In the old model, liquidity providers farmed tokens, sold them, and left. OlympusDAO wanted to own its liquidity rather than rent it. Therefore, the protocol allowed users to sell assets to the treasury for discounted vested token OHM. This process was called bonding because it mimicked the idea of buying a bond at a discount and redeeming it later at face value – except here, the “bond” paid out in OHM tokens rather than dollars. Users were incentivized to bond, because they were then able to stake OHM for astronomically high rebasing APYs. The idea was simple: when everyone cooperates, everyone wins — when participants defect, value collapses. OlympusDAO introduced in what was a very early form of the (3,3) cooperative game model that is now popularly utilized in Aerodrome/Velodrome forks. This became known as “DeFi 2.0.”

In this framing, OlympusDAO staking represents the optimal Nash equilibrium, denoted as (3,3), where mutual cooperation between users and the protocol compounds value through rebasing and autocompounding. Bonding, symbolized as (2,1), remains cooperative but asymmetrical: participants sell assets or LP tokens to the Olympus treasury in exchange for discounted OHM. This mechanism expands the protocol’s reserves and transitions liquidity ownership from mercenary farmers to the protocol itself, reducing external sell pressure. Selling, represented as (−2,−2), is the defection outcome where both the user and protocol lose as the reflexive flywheel of growth and trust unwinds.

From a mechanical perspective, bonding was OlympusDAO’s engine for Protocol-Owned Liquidity (POL). Instead of renting liquidity via temporary incentives, the protocol purchased it outright with newly minted OHM, vesting it to bonders over several days. When combined with staking, bonding created a powerful, though ultimately flawed and unsustainable, feedback loop: treasury growth reinforced OHM’s perceived backing, price appreciation encouraged further bonding, and staking amplified compounding.

However, the yield in OHM was purely inflationary, driven entirely by token minting without underlying revenue. The underlying fault with the OlympusDAO model was assuming that the sell case was truly (-1,-3), when it was in fact something closer to (2,-3). While a user could agree with others not to sell, there was no true incentive to do so and to deter defection. An individual holding had to trust that others would not defect and sell, where defecting had no true penalties, only potential lost gains. When inflows slowed, the same reflexivity that had driven growth reversed, leading to rapid contraction and a mass unwind of the (3,3) equilibrium. Thus, the OlympusDAO model was less a rigorous game theory backed design, and more so a risky coordination trust game.

While OlympusDAO’s (3,3) system gamified cooperation at the individual level, the next major DeFi era shifted that same principle of aligned incentives to the protocol level. The notion that collective participation could maximize shared value persisted, but its implementation matured. Instead of staking and bonding between users and a single treasury, coordination now centered on governance power and liquidity direction across protocols.

Curve Finance, launched in January 2020, had already become the backbone of stablecoin liquidity through its low slippage stableswap. In August 2020, the protocol introduced its vote-escrowed CRV (veCRV) system, liquidity itself became politicized via the (3,3) games. Holders could lock their CRV tokens for up to four years to receive veCRV, which granted voting power over which liquidity pools would receive emissions, boosts to personal yields, and a share of trading fees.

The introduction of Curve’s vote-escrow model (veCRV) reframed the idea of cooperation: rather than minting inflationary rewards, protocols competed for influence over Curve’s token emissions and incentives to the liquidity pools. Owning or influencing veCRV meant controlling yield, liquidity, and therefore market depth, particularly for the stablecoin liquidity. This meta-game of emission control became known as the Curve Wars. Dozens of protocols, from stablecoin issuers to yield aggregators, amassed veCRV or bribed its holders to direct emissions toward their pools, mirroring a more complex and capital-intensive form of OlympusDAO’s cooperative competition.

A pioneering example in the era of Curve Wars is the Convex Finance protocol launched in May 2021. Convex’s innovation was not a new AMM curve or token mechanic, but a governance aggregation layer. Instead of every protocol or individual locking CRV directly for veCRV, users could deposit their CRV into Convex, which performed the lock on their behalf and issued cvxCRV, a liquid derivative representing veCRV exposure. In exchange, Convex distributed boosted Curve yields, trading fees, and additional CVX token rewards, effectively socializing the benefits of long-term locking while abstracting away its complexity.

This model produced a reflexive flywheel similar in spirit to OlympusDAO’s (3,3) dynamics, but applied at the protocol-governance layer. The more CRV Convex locked, the more veCRV it controlled; the more veCRV it controlled, the more valuable its vote-direction services and CVX governance became. Within months, Convex had amassed over half of all circulating veCRV, consolidating a level of influence unprecedented in DeFi governance. Smaller DAOs that once competed directly for gauge votes, especially those who could not stand a chance of outvoting Convex any more, began instead to bribe or partner with Convex. This gave birth to a new layer of DeFi infrastructure, so-called “bribe markets” where governance votes became openly auctioned commodities.

Platforms such as Votium, Hidden Hand, and Redacted Cartel formalized what had initially been informal DAO-to-DAO side deals. In these systems, protocols deposited their own tokens or stablecoins into bribe contracts that rewarded holders of CVX (and later other vote-escrow tokens) for directing emissions toward specific pools. Each two-week gauge epoch on Curve turned into a recurring auction cycle, with participants competing for the most favorable yield-to-bribe ratios. The process became so systematized that data dashboards tracked “bribe APRs,” quantifying the value of each governance vote in real time.

Economically, this transformed Curve’s emissions from a fixed inflation schedule into a dynamic, market-priced coordination game. Gauge votes no longer merely reflected user preference for certain pools, but became a tradable asset class in their own right – the first liquid marketplace for DeFi governance influence. In doing so, bribe markets unlocked a second layer of yield for veToken holders: one derived not from trading fees or protocol performance, but from political demand for liquidity.

This meta-governance economy extended beyond Curve. Similar bribe mechanisms were adapted for other protocols implementing vote-escrow models, such as Balancer and Frax.

By early 2022, the Curve Wars had evolved into a fully-fledged governance economy, and like all economies, it eventually attracted superpowers. The final escalation came with the arrival of Terra’s UST and its alliance with Frax, which together launched the infamous 4pool initiative in April 2022. The goal was straightforward but audacious: to dominate Curve’s stablecoin liquidity by displacing the long-standing 3pool (DAI, USDC, USDT) as the network’s primary trading hub.

The 4pool combined UST, FRAX, USDC, and USDT, pairing the algorithmic stability of UST with Frax’s partially collateralized model and the liquidity of the two largest fiat-backed stablecoins, presenting a united front against DAI. Terra and Frax launched massive bribe campaigns across Convex and Votium, spending millions of dollars worth of tokens each epoch to capture gauge votes and direct emissions toward 4pool liquidity.

The 4pool impending dominance was abruptly stopped by the UST and Terra/LUNA collapse in May 2022, which tamed down the DeFi activity including the Curve Wars.

A massive step change in the yield space came with “The Merge,” comprising the Bellatrix and Paris upgrades on Ethereum in September 2022. The Merge changed Ethereum’s consensus protocol from a Proof-of-Work system, whereby validators provided hash power to mine blocks, to a Proof-of-Stake system, whereby validators provided stake to mine blocks.

In Proof-of-Work systems such as Bitcoin, hash rate (or computational power), is used to secure the blockchain. A simple explanation is as follows: any validator has the opportunity to “mine” a block. When we say “mine” a block, we mean the privilege to include transactions in a block and propose them to the network. But how do we ensure that a proposer honestly performs validity checks on transactions and proposes a valid block?

In Proof-of-Work systems, the validator’s likelihood to be selected as the proposer of a block is proportional to their hashrate relative to the hashrate of the network. As Bitcoin appreciates in value, the reward for proposing a block also appreciates in value, drawing more validators to try to mine the next block. This increases the network’s hashrate and makes it that, ceteris paribus to a validator’s hashing parameters, a validator is less likely to be selected as a proposer of the block.

The fault tolerance here comes from the fact that to attack the network, the computational power required to control a majority of the network’s hashrate for the 6 blocks required to finalize a block would be more expensive than the potential value from a successful attack of the network.

In contrast, Proof-of-Stake relies on “economic hashrate,” Rather than relying on the cost of computational power to secure a network, it relies on the economic cost of Byzantine, or malicious, behavior. To propose and validate blocks, a node must “stake” the native token, which is slashable in the event of dishonest behavior or poor performance.

Validators are rewarded in token emissions, proportional to their relative stake, for participating in consensus. Users who wished to stake but did not want to, or were not capable of, running a validation node themselves have the opportunity to delegate their stake to a node provider of their choice, who charge a fee and return the stake emissions to their delegators.

The original Ethereum staking design did not initially* support withdrawals: a user who staked ether had their ether “permanently” locked within the staking contract. Users who staked their ether would permanently be exposed to ether price movements via ether emissions. This incredibly rigid design led to the emergence of Lido and Rocket Pool, the first liquid staking protocols on Ethereum.

As implied by name, liquid staking protocols on Ethereum transformed a very illiquid staking design to a liquid staking design. Users who deposited into Lido or Rocket Pool essentially delegated their ether to Lido/Rocket Pool operators, and the protocol minted for them a 1:1 staked equivalent of their deposit (Lido’s stETH or Rocket Pool’s RETH). These staked derivatives represented their stake and automatically accrued staking emissions value, and unlike their native predecessors, were fully liquid and transferrable.

Suddenly, Ethereum exposure in staking became much more manageable. A user, worried about expected/current downward price trends of Ethereum, could offload their stETH/RETH and fully exit their ETH positions. The were other technical advantages of this way of “liquid staking” as well, primarily offloading the burden of reliably operating validators. Staking yields remains one of the most dominant forms of extracting yield from the market to date.

Tokens representing the staked tokens and their derivatives became popular as collateral in lending protocols, where the appreciation on the staking derivative from accrued staking emissions protected lenders to some degree from liquidation. In fact, in the early days of liquid staking, it was a common strategy to provide stETH as collateral to borrow ETH and safely loop staking yield, as the user would never be liquidated due to the collateral appreciating in value relative to the borrowed asset.

Other innovations included “liquid restaking” which further used liquid staking tokens to secure the logic of other protocols and networks against slashing conditions, such as Ethereum L2s, data availability layers, or in the case of EigenLayer, a validator with an abstract role that it needs to fulfill. Staking yield on those protocols is then accrued as value to the liquid restaking token (LRT) issued as a receipt for depositing the liquid staking token (LST). The restaking platforms such as Ether.fi, Puffer Finance, Renzo, Kelp DAO, Swell and others that emerged and rapidly grew at the end of 2023 and in the first half of 2024 follow the restaking narratives. Protocols like Lido and Rocket Pool exist today as well. They belong to the largest protocols by TVL, backed by “sustainable” protocol level economics.**

In traditional finance, parties are able to speculate on future yields by performing what is known as an “interest rate swap.” An individual, who possesses an interest bearing asset, sells the right to any future yields on this asset to another individual, who buys it at a fixed rate. We call this an “interest rate swap” because the individual who owns the asset swaps a “variable,” floating rate for a lump sum, which essentially constitutes a “fixed” rate.

An individual can be the buyer or seller of an interest rate swap for a multitude of reasons. Perhaps the seller thinks that the variable rate will decline and wishes to lock in a fixed rate that he/she believes will outperform the real, variable rate. Perhaps the seller is willing to take a slight loss on the overall rate for immediate, liquid access to the interest. On the opposite side, maybe the buyer thinks that the variable rate will outperform the lump sum the buyer pays to the seller as fixed yield.

Pendle emerged as a means to do the same on interest bearing assets in June 2021. It fully showed the impact of the DeFi winter, its TVL hovered around $15m USD in late 2022, but encountered explosive growth starting 2023 when integrating non-rebasing staking derivatives as well as new protocol mechanics. It further extended beyond staked assets to assets with speculative yield, such as tokens on protocols that are speculated to be involved in airdrops.

Pendle’s innovation separated the yield from staking into the principal (PT) and yield (YT) tokens. These tokens were further granularized by underlying yield (YT) and implied yield (IY). The underlying yield is that real, current yield of the asset (such as staking yield on stETH or basis yield on Ethena sUSDe). The implied yield is the yield implied by the price discovery of the asset on the Pendle market. For example, an increased demand for a yield token (YT), which guarantees rights of future yield of the underlying asset to the owner, increases the implied yield of that YT-asset on the market.

This tokenization which decouples principal from yield belongs, in our opinion, to one of the most fundamental DeFi mechanics as it allows for the creation of advanced products with adjusted parameters. For example, exchanging tokenized yield for increased security of the underlying principal.

*Withdrawal functionality would only be added later in the Shanghai/Capella upgrades in mid-2023. Native withdrawals, while an improvement over permanently locked stake, were still subject to unbonding periods that varied depending on the amount of tokens being unbonded at the time of unbonding.

**It’s important to note that this has also caused concern that consensus was becoming increasingly centralized. If desired, Lido and Rocket Pool could theoretically collude to attack Ethereum, as together they comprise a ~1/3 of total stake in Ethereum, where Ethereum requires 2/3 honest stake to be fault tolerant. This is unlikely, however, as the protocols’ primary source of value is the staked ETH they secure. Regardless, there have been proposals to disincentivize centralized liquid staking by reducing emissions for large staking pools.

Looking back at the evolution of yield, the pattern is clear. All major leaps forward have been classified by a 0-to-1 innovation that has either simplified user experience or unlocked capital efficiency. Manual lending on EthLend was automated better by Compound and later abstracted away by automated reallocation on Yearn and other aggregators. Complex governance optimizations in the Curve Wars were streamlined by meta-protocols like Convex. Staking inconveniences, their capital inefficiencies, and their technical overheads were addressed by liquid staking tokens (LSTs) and their yield-bearing design. So what comes now, and how can the DeFi protocols and developers innovate in the years to come?

It’s evident that 2025’s DeFi looks vastly different from its emerging days. DeFi, and the industry as a whole, has undergone tremendous growth: Total Value Locked (TVL) in DeFi protocols has grown from just ~USD$1B prior to DeFi Summer to ~USD$150B as of today. Today, DeFi is massively complex, extending far beyond the simple lending, borrowing, and liquidity provisioning of the 2018 – 2020 era. DeFi’s core value proposition remains the financial freedom to operate in the P2P economy money markets without intermediaries, but realizing this now requires navigating bridging risks, managing positions across different chains with different architectures and user experiences, and assessing unfamiliar risk profiles. The challenge for DeFi users is not finding yield but coordinating it.

Similarly, the bottleneck is no longer the lack of yield opportunities or adoption: DeFi is more mature than ever, bleeding into TradFi and vice versa. ETFs are beginning to deploy TradFi funds into staking, while DeFi vaults diversify into TradFi yields such as tokenized treasuries and private credit. Web3 now has ~USD$300B in stablecoin market capitalization across numerous variants, powering everything from global payments to on-chain yield strategies.

The next successful applications will likely follow this same formula: abstracting friction, unlocking idle capital, and reimagining financial primitives. The builders who can combine the existing ingredients will create genuinely novel products. The existence of a universe of blockchains – networks with unique value propositions, such as unparalleled capital depth, unmatched speed or cost efficiency, hardened security, or privacy, each with varied DeFi offering, are turning pain points into opportunities, thanks to maturing interoperability standards. AI agents can begin optimizing strategies and autonomously reallocating capital across chains in real time. Composability now extends not only across blockchains but across entire computational paradigms. DeFi may evolve into an autonomous layer of the global financial system, operating continuously and transparently across human and machine participants.

An underexplored area of on-chain finance appears to be credit scoring. Unlike in traditional systems, blockchain users lack persistent identity and reputation. Defaulting to an on-chain loan carries no long-term consequence because one can continue operating under a new address – an identity, with no former history. The disconnect between on-chain identity and real-world personal credit system is a structural challenge but also one of the most imminent frontiers for innovation. Projects that can integrate verifiable identity, credit data, and decentralized capital markets could redefine undercollateralized lending on-chain altogether.

Security challenges persist in DeFi in 2025 as well. It is estimated that over $2.5 billion were lost to protocol exploits, phishing, and orchestrated scams this year alone. We can observe an increase in the losses related to the increased engagement of the general retail audience with web3, but we also continue to see organized groups executing sophisticated attacks, such as the recent attempts to weaponize web3 application frontends. The operators of on-chain products will have to face these evolving needs.

DeFi’s story is still being written. Its early chapters were about yield. Its current chapters are about yield and integration. Its next chapter will be about yield, integration, and intelligence. The opportunity to innovate has never been greater, and the future of open on-chain finance is only beginning. We are witnessing a true financial revolution.