DeFi vaults are smart contracts that automatically manage your yield strategies. Instead of manually jumping between protocols, signing dozens of transactions, and tracking rates, a vault handles everything for you. Without one, you'd be selecting protocols, approving transactions, monitoring rates, claiming rewards, swapping tokens, and reinvesting. Each step costs gas and time. A vault turns this into a single deposit that compounds automatically. Your wallet holds the position, the vault keeps your capital productive.

The way vaults operate is simple and intuitive. The process follows a clear flow that shows how capital moves, generates yield, and compounds over time, for example

With repeated cycles, returns compound and your shares become redeemable for a larger amount of the underlying asset.

If the strategy performs well, the value of each share increases relative to the underlying asset. If it performs poorly, it decreases. You can always check how much of the base asset your shares are currently worth.

Another useful point is to understand the difference between APR and APY.

APR is the annual rate without reinvestment. APY is the effective annual rate after reinvestment. Vaults that compound frequently usually report APY, since compounding is central to the experience.

The main advantages come from this design:

Vaults are particularly well suited on Zircuit, where low fees and fast settlement align well with the needs of yield vaults that require frequent and efficient compounding.

Before diving into vault strategies, it's important to understand the building blocks they use. Most vaults don't start from scratch, they build on assets that already generate yield. These yield-bearing tokens form the foundation of more complex strategies.

Lending stablecoins underpins many vaults. The key distinction is how interest shows up in your wallet: rebasing versus non-rebasing.

Rebasing tokens

An example is Aave aTokens. When you supply USDC you receive aUSDC 1:1 and your aUSDC balance increases as interest accrues. This is intuitive for users because the number in the wallet grows. In vault design it complicates accounting and compounding logic, tends to be less gas efficient due to the rebasing mechanics, reduces composability with other contracts, and increases the surface for implementation errors.

Non-rebasing tokens

An example is Compound cTokens. When you supply USDC you mint cUSDC and the cUSDC balance stays constant while the exchange rate to USDC rises over time. This structure is easier to integrate into vaults, is generally more gas efficient, and is more composable across protocols because balances do not auto-change.

Why this matters for vaults

Since a vault abstracts balances from end users, intuition at the wallet level is less important than operational efficiency. Non-rebasing tokens usually fit vaults better because they simplify accounting, improve composability, and align with the goal of minimizing execution costs.

However, protocols such as Morpho operate on top of these markets to improve capital efficiency. They try to match lenders and borrowers directly within each market so that both sides receive better rates. When a match occurs, the lender earns a rate between the pool’s supply and borrow rates, and the borrower pays below the borrow rate. If no match occurs, the position reverts to the base pool (Aave or Compound for example), preserving liquidity and risk parameters.

For vaults, this is particularly advantageous because small improvements in the supply rate, applied to large balances and repeated over multiple compounding cycles, can noticeably increase net returns.

Liquid staking applies the same principle to proof-of-stake assets.

With Lido, for example, you stake ETH and receive stETH, which represents your staking position plus validator rewards. Many applications prefer wstETH, a wrapped version whose balance does not rebase. Instead, 1 wstETH becomes redeemable for more ETH over time.

The advantage is capital efficiency: you continue to earn staking rewards while being able to use the liquid version as collateral or in other strategies.

Alternatives like rETH and cbETH follow the same principle, with different operators and mechanisms. In vaults, these tokens act as productive base assets similar to interest-bearing stablecoins. Because LSTs are highly liquid and composable, they also serve as diversifiers that let vaults pursue higher risk strategies while maintaining efficient collateral and routing.

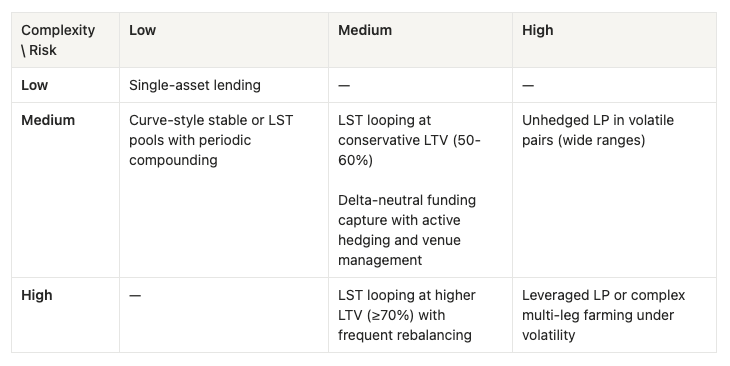

Now that you understand the underlying assets, let's look at how vaults actually put your capital to work. Each strategy has its own risk-return profile, and choosing the right one depends on your goals and risk tolerance. To orient the reader, here is a quick map of strategies by complexity and risk.

Strategy: Low Risk, Low Complexity

As the low-complexity, low-risk baseline, this vault supplies stablecoins to a major money market and auto-compounds interest. Rates follow utilization and incentives and typically sit in the low to mid single digits under stable conditions. There is no borrowing leg or liquidation path, making it a straightforward way to learn deposits, shares, and withdrawals while seeing compounding in action.

Strategy: Medium/High Risk, Medium Complexity

Looping, or recursive lending, amplifies yield when the return on collateral exceeds the cost of borrowing or when incentives create a positive spread. The basic idea is to deposit collateral, borrow against it, convert the borrowed asset back into the collateral form, and redeposit. This process is repeated until the system reaches a stable equilibrium defined by a target health factor (HF).

In practice, this is most efficient with liquid staking tokens (LSTs) such as wstETH (wrapped staked ETH). The reason is structural: your collateral (wstETH) represents staked ETH that accrues yield, while your debt (WETH) represents plain ETH that does not. Because wstETH continually appreciates relative to ETH as staking rewards accrue, your collateral base appreciates over time while your debt remains constant, meaning the position naturally improves in health instead of deteriorating. This is what makes the wstETH-WETH loop uniquely attractive compared to same-asset loops.

Why borrow WETH against wstETH?

In a normal pooled lending market, supply APY < borrow APR, so looping the same token (e.g., USDC → borrow USDC → redeposit) just increases leverage and risk without increasing yield. The borrow cost always eats the supply return, making the spread negative.

But in the wstETH-WETH pair, the collateral’s value drifts upward relative to the borrowed asset. Each wstETH token represents slightly more ETH over time due to staking rewards, so the effective supply APY exceeds the borrow APR even if nominal rates look similar. The result is a structurally positive carry, which means that you earn staking yield on a growing wstETH base while paying a fixed-rate ETH borrow.

The only condition required for this to hold is that the wstETH-ETH peg remains stable, which it typically does, and that borrow rates do not spike above staking yield for prolonged periods.

After a few iterations on your wstETH, you earn staking yield on a larger wstETH base while paying the borrow rate on the WETH debt. The net return is approximately the staking APY times the effective leverage minus the borrow APR minus swap costs and fees. The realized outcome depends on interest rates, price volatility, slippage, and how often the position compounds.

Numerical example (wstETH loop at 70% LTV):

Actual results depend on rates, slippage, price volatility, and compounding frequency.

Risk management is essential: the same leverage that boosts yield also increases downside risk. Keep a healthy buffer below the liquidation limit. If the maximum LTV is 70%, operating around 60 to 65% reduces stress during volatility.

Adding Morpho can make looping more efficient. When supplied balances are matched peer to peer, they earn slightly above the pool’s supply rate, and when loans are matched, they pay slightly below the pool’s borrow rate. These small edges compound into a higher overall APY, and any unmatched portion simply reverts to the base pool, preserving liquidity access.

This looping pattern also applies to liquid staking tokens. Structured products built on wstETH use the same mechanism to amplify staking rewards. The logic is the same as above, with the added consideration of ETH price volatility, which the vault must buffer or hedge.

Why borrow against wstETH and hedge with a wstETH short instead of borrowing a stable or a yield-bearing stable?

Strategy: Medium/High Risk, High Complexity

Vaults can generate yield by providing liquidity on decentralized exchanges, capturing trading fees and protocol incentives. The mechanics vary by platform, but all LP strategies must balance fee income against price risk:

Uniswap (non-stable pools)

Concentrated liquidity allows capital to be positioned in the most active price ranges. The strategy improves fee capture but requires careful management of price ranges. The vault monitors volatility, adjusts ranges, and compounds fees periodically. The main risk is impermanent loss. When the relative price of assets in a pool changes, the LP position diverges. This can cause the position to underperform compared to simply holding each asset. The strategy logic aims to balance fee income with price variation (drift).

Curve (stable pools)

Vaults often allocate to pools that combine stablecoins or liquid staking tokens, where prices are tightly correlated. The vault collects fees, claims protocol incentives, and periodically sells them to compound the position. Lower volatility and the stableswap invariant improve execution quality: deep liquidity around the peg reduces slippage and price impact compared with constant-product AMMs, so returns are typically more stable.

Strategy: Medium Risk, Medium Complexity

Delta-neutral strategies aim to keep price exposure near zero while collecting predictable sources of return. A common form, known as basis trading, profits from the basis, which is the price difference between the perpetual and spot markets. This is expressed through the funding rate mechanism designed to close that gap.

Funding rate

Perpetual futures do not expire. To keep the perp price close to spot, exchanges apply a periodic funding payment between traders. When the perp trades above the spot index, longs pay shorts. When it trades below, shorts pay longs. The rate updates on a schedule and can change sign as market conditions shift.

Canonical setup

Hold a long exposure to ETH, for example spot ETH or staked ETH, and open a short position of equal notional in an ETH perpetual. Price moves are hedged. The remaining PnL comes from funding payments on the short plus any base yield on the long leg, for example staking rewards on wstETH or lending interest on posted collateral.

Other delta-neutral variants

Simple example

Suppose staking APY on wstETH is about 5% and the average funding received on a short ETH perp is about 6% annualized. Ignoring fees and slippage, the gross carry is about 11% before costs. If funding flips negative for a period or if borrow and trading fees rise, the net carry falls accordingly.

Risks and controls

Key risks include funding rate flipping sign, liquidity and execution costs on the perp venue, collateral management and margin calls, oracle and venue risk, and basis variance between the perp index and the asset you hold, for example a temporary discount on stETH. Additional threats include Auto-Deleveraging (ADL), where profitable positions can be force-closed to offset losses of liquidated traders during extreme volatility (as seen on October 10th, 2025), and adversarial targeting on public ledgers, where large or predictable positions may be front-run, hunted, or otherwise exploited by on-chain actors. A well-engineered vault enforces strict health thresholds, rebalancing logic, and pause conditions to maintain safety within defined guardrails.

Who is this for

Users should understand the risk profile and what drives returns, but they do not need to manage the mechanics. The purpose of the vault is to abstract the monitoring, re-hedging, and risk controls so depositors get a neutral carry stream with clear disclosures on parameters and limits.

Some vaults have privileged roles such as strategist, pause guardian, or an upgradeable admin. These roles can change parameters, pause the strategy, upgrade contracts, or adjust fees. The benefits are faster response and safer emergency actions, but they introduce operator and key-management risk. Mitigations include clear role disclosures, time-locks on upgrades, multi-sig control, on-chain caps and circuit breakers, and transparent policies for pauses and withdrawals.

Smart contract risk is the most visible. Even mature protocols can have bugs, and each integration adds complexity. Audits, public monitoring, and time in production help but never eliminate risk.

Protocol risk runs deeper. Money markets depend on oracles, liquidation engines, and market depth. Under stress, failures in pricing or thin liquidity can spike rates and trigger cascades. A recent October 2025 stress event showed how engines that referenced internal books instead of multi-source, depth-weighted oracles saw prices diverge sharply across CEXs and DEXs, accelerating liquidations. This is especially relevant for vaults that use looping or leverage.

Vaults that hold aTokens or cTokens are only as strong as their underlying markets. Liquid staking tokens depend on validator performance and slashing rules and can trade at a discount during stress, which matters if the vault must exit quickly. Practical mitigations include multi-venue oracle aggregation, TWAP and outlier filters, conservative LTV buffers, and pause conditions when spot-index divergence exceeds predefined thresholds.

Strategy risk grows with each additional leg. Single-asset vaults have few moving parts. Looping vaults depend on the supply-borrow spread and collateral stability. LP vaults depend on trading volume and price behavior. Delta neutral vaults depend on derivative funding and the ability to maintain hedges. These risks are manageable but must match your experience level.

Liquidation risk deserves special attention. Any strategy that borrows against collateral must maintain buffers and have a deleverage plan for fast markets. Protection mechanisms include:

Diversifying across strategies and protocols further reduces the impact of isolated events.

Vaults bring professional yield management to anyone with a wallet. They handle routing, harvesting, and compounding while providing clear share tokens that track your claim on the strategy.

Start with a simple position to see the mechanics in action. A single-asset lending vault is a good first step. Once you feel comfortable with deposits, shares, and withdrawals, explore looping when spreads support safe leverage.To explore further, LP and delta neutral strategies can add new, relatively safe sources of yield if risk is properly managed.

The common theme is understanding, not blind trust. Read the strategy, check the underlying protocols, and know which parameters drive returns and which thresholds trigger adjustments. With that mindset, vaults become more than a convenience. They offer a disciplined and scalable approach to managing yield.

Want to dive deeper? Explore the Zircuit documentation, join our Grants Program with vault ideas, or connect with the team to discuss integrations and use cases.

Until next time,

The Zircuit Team 💚