In May 2022, Terra's UST was the third largest stablecoin in cryptocurrency, holding over $18 billion in circulation. Nine days later, it traded below one cent. That collapse erased more than $45 billion in market value and triggered a cascade of failures across the crypto lending industry. Three Arrows Capital, Celsius Network, Voyager Digital, and BlockFi all fell within months. The contagion froze billions in customer assets and sent multiple executives to prison.

Three years later, the pattern repeated. In November 2025, Stream Finance disclosed a $93 million loss that spread across $285 million in interconnected DeFi debt. Its stablecoin xUSD lost over 90% of its value in 48 hours. Elixir Network's deUSD collapsed 98%. Lending protocols scrambled to contain the damage.

The total cost of major protocol failures since 2022 now exceeds $60 billion. These were not random accidents. Each collapse shared recognizable warning signs: yields that defied market logic, collateral structures that referenced themselves, and concentration risks that turned single failures into systemic crises.

This article examines the three most significant waves of crypto protocol failures. It analyzes the business model flaws behind Terra's algorithmic stablecoin, the uncollateralized lending practices that brought down the 2022 lenders, and the hybrid opacity that destroyed Stream Finance. More importantly, it provides a practical framework for identifying these risks before they materialize.

The lessons cost billions to learn. Understanding them costs only your attention.

Terra's UST promised something revolutionary: a stablecoin that maintained its dollar peg through pure mathematics rather than reserves. The mechanism was elegant in theory. Users could always exchange one dollar worth of LUNA tokens for one UST, and vice versa. Arbitrage would keep the price stable. No banks, no vaults, no counterparty risk.

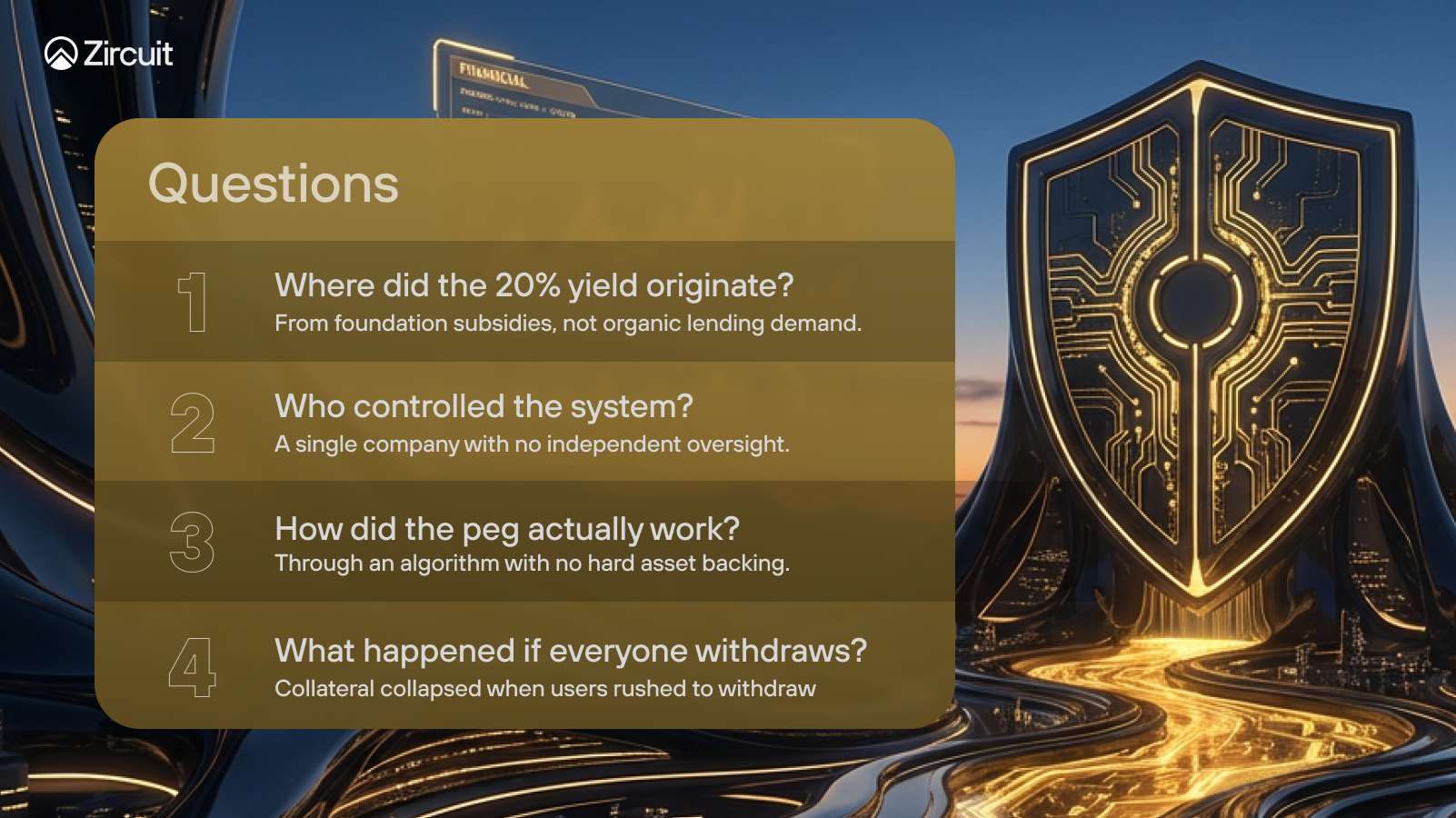

Anchor offered 19.45% annual yield on UST deposits, a rate that dwarfed anything available in traditional finance or even competing DeFi platforms. This yield attracted capital at an extraordinary pace. By May 2022, Anchor held $17.15 billion in total value locked and contained 72% of all UST in existence. A single protocol had become the entire reason most people held the stablecoin.

That concentration created a fatal dependency. The yield was not sustainable. Terraform Labs had injected $450 million into Anchor's reserves just months earlier to maintain the advertised rate. When confidence wavered in early May, withdrawals from Anchor exceeded the system's capacity to absorb them. UST began trading below its peg. The arbitrage mechanism that was supposed to restore stability instead triggered a reflexive death spiral.

As UST holders rushed to redeem their tokens for LUNA, the protocol minted new LUNA to meet demand. More LUNA meant lower prices. Lower prices meant more minting. The supply exploded from 350 million tokens to 6.5 trillion in days. By May 16, UST traded at two cents and LUNA was effectively worthless.

The warning signs were visible to anyone asking the right questions:

Do Kwon, Terra's founder, fled to Montenegro with a forged passport after the collapse. In August 2025, he pleaded guilty to fraud charges. Prosecutors requested a fifteen year sentence, describing losses that exceeded even the FTX collapse in scale.

But Terra's destruction did not end with its own investors. The collapse triggered margin calls across the industry, and the firms that could not answer them would fall next.

The margin calls arrived within days of Terra's collapse, and Three Arrows Capital could not answer them.

Three Arrows, known as 3AC, had grown into one of crypto's most influential hedge funds, managing approximately $10 billion in assets at its peak. The fund's co founders, Su Zhu and Kyle Davies, had built their reputation on leveraged bets across the ecosystem. They held significant exposure to Terra, with an estimated $600 million in LUNA and UST positions. When those positions went to zero, 3AC's lenders wanted their money back.

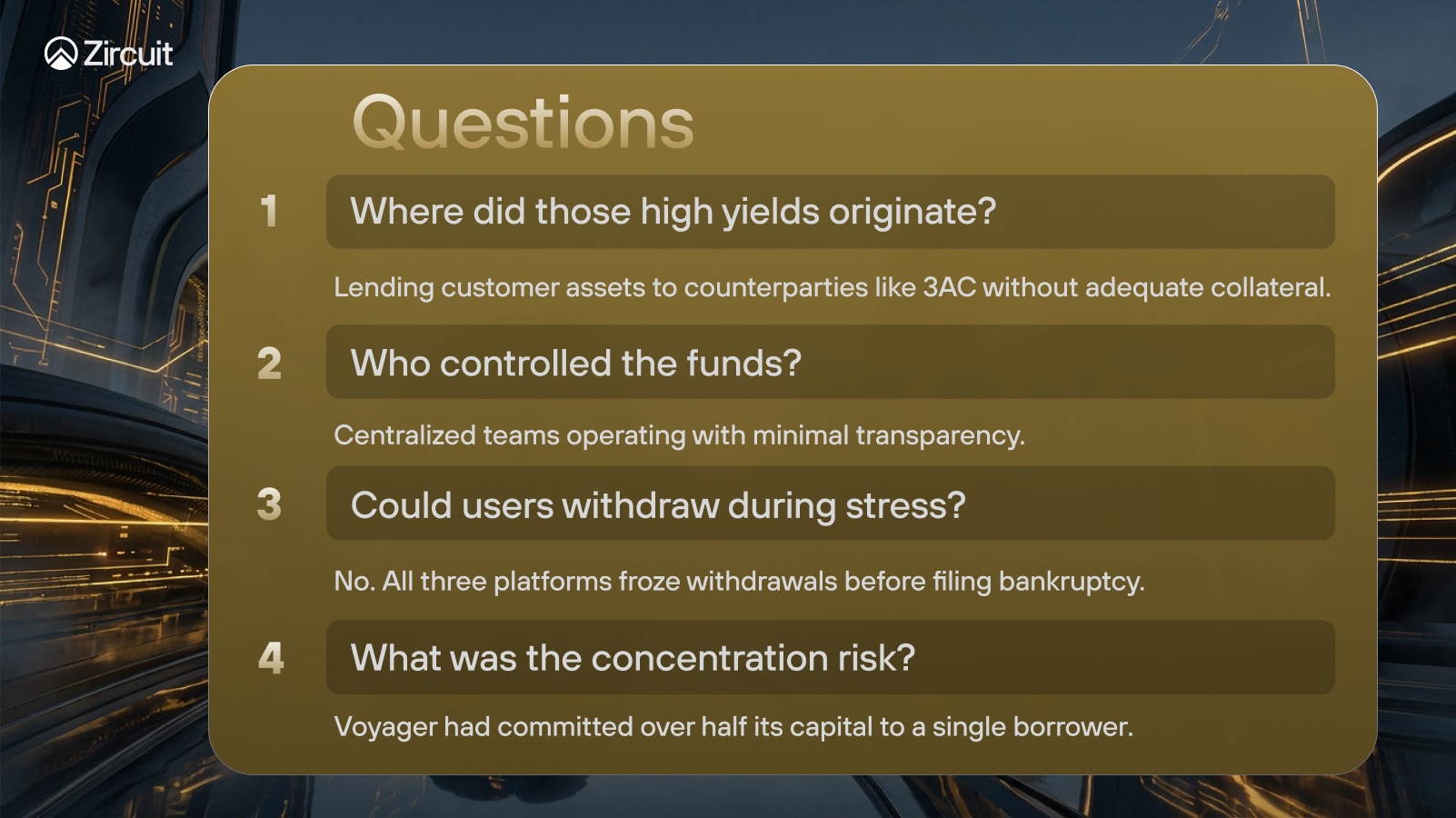

The fund owed $3.5 billion to 27 different creditors. Among them was Voyager Digital, which had extended a loan worth $670 million in Bitcoin and USDC to 3AC. That single loan represented more than half of Voyager's entire loan book. When 3AC defaulted, Voyager's fate was sealed.

But Voyager was not alone in its exposure to poorly collateralized lending.

Celsius Network had positioned itself as "not a bank" of crypto, promising retail investors yields as high as 17% on their deposits. The platform's founder, Alex Mashinsky, marketed Celsius as safer than traditional banks while his company made uncollateralized loans and speculative investments with customer funds. At its peak, Celsius held $25 billion in assets. When withdrawals accelerated following Terra's collapse, Mashinsky assured customers that their funds were safe. Days later, Celsius froze $4.7 billion in customer accounts.

The dominoes fell rapidly. 3AC filed for bankruptcy on June 27. Voyager followed on July 6. Celsius filed on July 13. Within six weeks, three major platforms had collapsed, and 1.7 million Celsius users alone could not access their funds.

The failures shared a common architecture.

The aftermath brought accountability. Mashinsky pleaded guilty in December 2024 and received a twelve year prison sentence in May 2025. Su Zhu served four months in a Singapore prison for refusing to cooperate with liquidators. Voyager creditors recovered between 50% and 72% of their claims. Celsius achieved a 93% recovery rate by March 2025.

One platform defied the pattern entirely. BlockFi, despite filing bankruptcy in November 2022, ultimately returned 100% of customer claims by selling its FTX settlement at a premium. The difference was asset management and transparent recovery processes.

The industry believed it had learned. Regulations were proposed. Risk frameworks were discussed. Three years passed. Then, Stream Finance proved that the lessons had not taken hold.

Three years of industry reflection produced new terminology but familiar failures. Stream Finance collapsed in November 2025, proving that wrapping old risks in new language did not eliminate them.

Stream operated as a "CeDeFi" protocol, a hybrid model that combined decentralized token infrastructure with centralized fund management. Users deposited USDC and received xUSD, a yield bearing token that promised returns through "institutional grade" strategies. The protocol reported $520 million in assets under management and offered yields around 18% annually. The actual user deposits totaled approximately $160 million. The difference was leverage.

On November 4, 2025, Stream disclosed that an external fund manager had lost $93 million of platform assets. The announcement triggered immediate panic. Within 24 hours, xUSD plummeted from one dollar to 26 cents. By the end of the week, it traded between 7 and 14 cents, a decline exceeding 90%.

The damage spread instantly through interconnected protocols.

Elixir Network had lent $68 million to Stream, representing 65% of the reserves backing its own stablecoin, deUSD. When Stream froze withdrawals, Elixir could not honor redemptions. deUSD collapsed 98%, falling from one dollar to less than two cents. The project shut down entirely.

Lending protocols faced a different problem. Platforms including Euler, Morpho, Silo, and Gearbox had accepted xUSD as collateral for loans. When xUSD lost its value, those loans became undercollateralized. However, several protocols had hardcoded xUSD's oracle price at one dollar to prevent cascading liquidations during normal volatility. That safety mechanism became a trap. The system still valued worthless collateral at full price, preventing automatic liquidations and leaving lenders with $137 million in bad debt on Euler alone. Total exposure across all affected protocols reached $285 million.

The red flags preceded the collapse by months. Where did 18% yield originate? From an external fund manager whose strategies were not visible on chain. Who controlled the assets? A centralized team with no transparency dashboard. What backed xUSD? Circular collateral structures where xUSD backed deUSD and deUSD exposure fed back into xUSD. Could users exit during stress? No. Withdrawals froze immediately after the loss announcement.

Compound Finance acted decisively, pausing affected markets before contagion could spread further. That intervention prevented a broader crisis but could not recover what was already lost.

What Stream's Collapse Actually Proved:

The CeDeFi model, combining centralized management with decentralized infrastructure, is not inherently broken. The problem was not that Stream used external fund managers. It was that those managers operated without regulatory oversight and without meaningful accountability structures. The centralized components lacked every safeguard that makes centralization tolerable in traditional finance: regulatory licensing, mandatory reporting, auditable operations, and real consequences for misconduct.

This distinction matters. A hybrid model where the centralized components operate under FCA or CFTC oversight, with verifiable track records and real-time exposure reporting, would address the specific failures that destroyed Stream. The question is whether the industry will build those safeguards or simply rebrand the same opacity again.

The patterns from 2022 had returned with new names. Unsustainable yields, opaque management, circular dependencies, and concentrated exposure. The lesson was the same. The tuition was just as expensive.

The same failures kept repeating because the same warning signs kept being ignored.

Across Terra, the 2022 lenders, and Stream Finance, four patterns appeared consistently. Recognizing them is the difference between avoiding catastrophe and becoming part of it.

Unsustainable Yields

Terra's Anchor offered 20% when comparable protocols paid 4%. Celsius promised 17% while making uncollateralized loans. Stream advertised 18% through opaque external managers. In each case, the yield exceeded what the underlying business model could generate. For comparison, established curators like Steakhouse and Gauntlet were offering 5-6% on similar strategies. When a protocol promises three times that rate, the question is not whether it will collapse but when.

Circular Collateral

Terra's UST was backed by LUNA, whose value depended on demand for UST. Stream's xUSD backed Elixir's deUSD, which had 65% of its reserves exposed to Stream. These self referential structures create the illusion of stability while amplifying risk. When one element fails, everything fails simultaneously.

Concentration Risk

Anchor held 72% of all UST in existence. Voyager committed over half its loan book to a single borrower. Elixir placed 65% of its reserves with one counterparty. Diversification is not optional in asset management. Single points of failure become single points of collapse.

Opacity Over Transparency

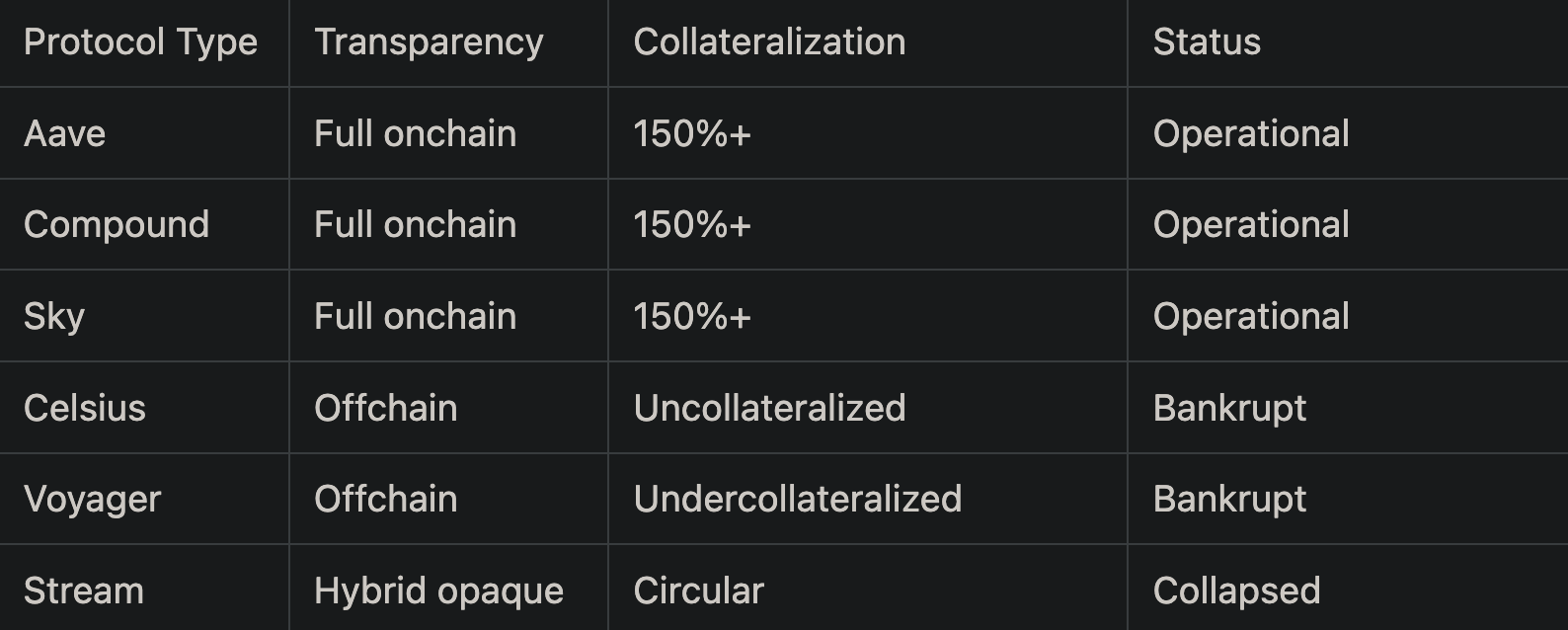

The protocols that survived 2022 shared common characteristics. Aave, Compound, and Sky (MakerDAO) operated with full on chain transparency, overcollateralized positions, and algorithmic liquidations. The protocols that collapsed operated with centralized control, off chain strategies, and minimal disclosure. Stream Finance exemplified this opacity: its founder remained pseudonymous, the external fund manager was never identified by name or agreement, and capital management occurred entirely offchain. The pattern is unambiguous.

The evidence is not subtle. Transparency and overcollateralization correlate directly with survival. Opacity and leverage correlate directly with failure. The next section examines how regulations are beginning to codify these lessons into law.

Regulators watched $60 billion disappear and responded with legislation designed to prevent the next collapse.

The European Union moved first. MiCA, the Markets in Crypto Assets regulation, took full effect on December 30, 2024. The framework requires stablecoin issuers to maintain reserves at a strict one to one ratio with liquid assets. Algorithmic stablecoins like Terra's UST are effectively banned. Monthly audits and public disclosure of reserve composition are mandatory. The rules that could have prevented Terra's collapse are now law across 27 countries.

The United States followed seven months later. President Trump signed the GENIUS Act on July 18, 2025, establishing the first federal framework for payment stablecoins. The legislation mandates 100% reserve backing in US dollars or short term Treasury securities. Issuers cannot offer yield or interest on stablecoin holdings. In bankruptcy, stablecoin holders receive priority over all other creditors. Violations carry penalties up to $1 million per incident and five years imprisonment.

These regulations share a common philosophy: if a stablecoin cannot prove its backing in real time, it should not exist.

But regulation addresses only half the problem. The Stream Finance collapse revealed another critical failure: lending markets built on top of yield bearing assets need sufficient liquidity to absorb stress. Morpho markets with xUSD exposure were fully drained during the crisis, leaving lenders unable to exit and losses socialized across all participants. When collateral fails and liquidity disappears simultaneously, even well intentioned protocol design cannot prevent contagion.

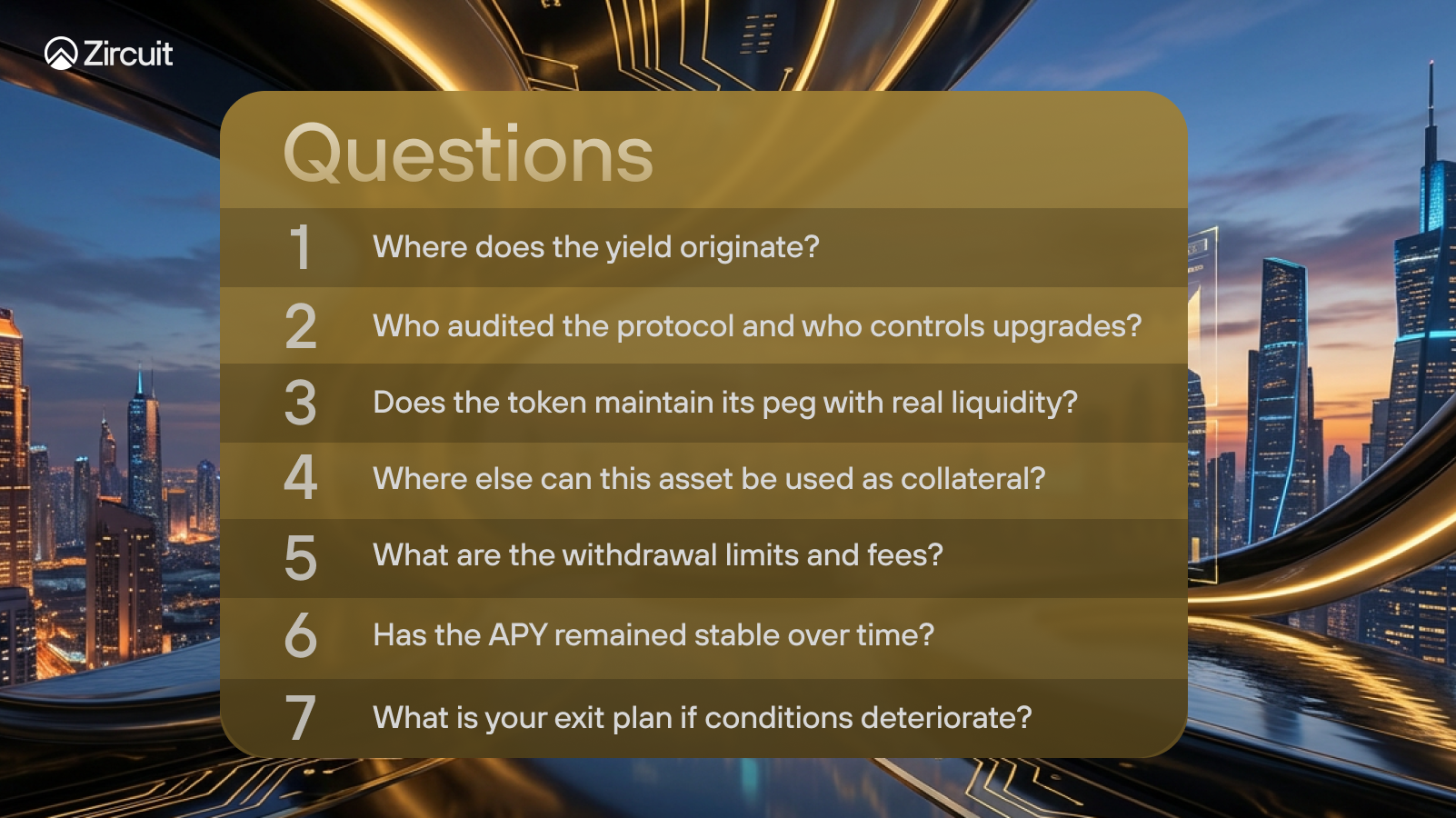

Regulation and protocol design both matter, but neither can fully protect individual investors. The 7-step due diligence framework applied throughout this article provides a practical filter for evaluating any yield generating protocol:

The protocols that failed could not answer these questions satisfactorily. The protocols that survived could. The framework is simple. Applying it consistently is the challenge.

Nine days separated Terra's $45 billion peak from total collapse. Six weeks separated Three Arrows Capital's default from an industry wide crisis. Forty eight hours separated Stream Finance's disclosure from a 90% loss in xUSD value.

The speed of collapse leaves no room for reaction. The only protection is preparation.

More than $60 billion in losses now document what happens when investors ignore unsustainable yields, circular collateral, concentrated exposure, and opaque management. The patterns are not hidden. They repeat because people refuse to look for them.

The 7 step due diligence framework exists to change that pattern. Before allocating capital to any yield generating protocol, answer every question. If the protocol cannot provide clear answers, your capital does not belong there.

The infrastructure that survives the next crisis will be the infrastructure that studied what destroyed its predecessors: regulated counterparties, transparent operations, verifiable accounting, and architectural resilience that does not depend on market conditions remaining favorable. That infrastructure is beginning to emerge. The question for investors is whether they will demand it before the next collapse, or after.